Resolving the Green Paradoxes: Thriving Under Energy Transition Uncertainties

Popular enthusiasm for variable renewables,

particularly for solar power of late, is unmatched by the adopting firms’ parlous financial performance. Growth does not often translate into profits, and China and the United States account for more than half of global installations. Germany and Spain, erstwhile leaders, make up the European story, with Denmark carving a niche with its technological leadership.

Still, wide scale variable renewables deployment remains elusive, in spite of generous subsidies. In fact, the default policy mantra, “Subsidize your way to decarbonize the economy,” seldom delivers, yet lenders follow suit by limiting funding to coal-fired power assets. With these twin actions, one would think we would have the wind and the sun energize our economies—but they do not.

Part of the problem lies in how renewables are valued as individual projects, rather than as part of a portfolio of diversified supplies. Recognizing variable renewables’ higher costs, subsidies equalize the costs differences following grid price parity principles. While the costs difference between variable renewables and gas (ACCGTs) or coal (Coal) are easy to calculate, the answers are indeterminate. Renewables’ costs are generally stable given their zero fuel costs. However, costs of gas or coal vary frequently with the energy markets. The rest is math: When stable renewables’ costs are deducted from volatile fossil fuel costs to derive a “correct” subsidy, multiple answers result. Therefore, subsidies set under presumed constant prices would over- or undercompensate renewables. With this uncertainty, subsidies seldom lead to wide scale deployment, resulting in a green paradox.

The persistence of green paradox, and its causes, are far from obvious. in my new book— Energy Investments: An Adaptive Approach to Profiting from Uncertainties—I posit the following counter-intuitive propositions:

- Subsidies embed risks, rather than secure cash returns of investors.

- Take-or-pay, or power purchase agreements, increase financial risks from continual renegotiations.

- Rapidly declining solar costs reward late adopters, hence encouraging deferral of investments.

Capital budgeting’s preference for predictability is a culprit. Variations are frowned upon as risks that should be minimized by fixing the prices or volumes. When markets are volatile, erroneous decisions result. Just because financial analyses chose to ignore volatilities, and its effects on feasible outcomes, does not make dynamic energy markets less volatile.

Flawed Logic Requires Reframing

Let us start by understanding the nature of the beast we are dealing with.

There are two types of renewables. Modulated hydro (StoHydro) and geothermal (Geo) enjoy high utilization rates with flexibility to adapt supplies to fluctuating demand. The other is variable renewables such as wind (OnsWind) and solar (PV) characterized by intermittent supplies with no flexibility on volumes. Both benefit from zero fuel costs and minimal operating expenses. Low volume utilization, however, render variable renewables expensive on a life cycle cost of energy (LCOEs) basis, notwithstanding the sharp falls since 2010. Power storage offers hopes to remedy solar power’s shortcomings. However, expensive supply stored in high cost storage may not result in competitive energy supply, even if flexibility is enhanced.

Net present value (NPV) is capital budgeting’s staple tool. Conceptually, expected cash flows over the life of the project are discounted to today’s value with their sum giving the payoffs. A sum is invested to build the assets so that payoffs could be earned. By deducting what was invested from the payoffs, the excess value accrues to the investors, or the NPVs. When NPVs are positive, the projects with highest NPVs get the cash first, followed in rank order by the next projects.

Managers, however, operate under volatile energy markets that wreak havoc on NPV’s wellordered world. What is attractive when prices are as forecasted may be a dud when markets become adverse. Without the flexibility to reverse decisions, or adapt operations or supplies to changing market conditions, managers could only watch their hoped-for payoffs dissipate. The common refrain becomes “unexpected” market moves “surprised” the managers, hence losses that were “not anticipated”.

Trusting in subsidies’ longevity, managers entrust their fate to the integrity of the legal framework. However, policy hardly possess the omniscience to know how costs, much less how technologies would evolve. By picking a “champion,” policy proceeds to “copy and paste” subsidies applied across markets. The consequence? What worked in Spain for a while failed in Romania despite its more generous payments at the starting block. Belatedly, policy realized the differences in markets, its needs, and what works (or not).

This is where understanding how market structures influence outcomes matters, but they are often ignored by managers and policy. The concept of pre-emption by rivals, and its influence on timing the investments, are the core of strategy formulation. However, its importance is lost when finance takes over the work of evaluating the investments and competing opportunities. Hence, there is a strategy disconnect that breaks a supposed nexus for thriving firms.

Moreover, monopolists face no threat of pre-emption by credible players. To induce a monopolist to invest, subsidies will have to be substantially high. They have the luxury to wait until prices are very high, possibly caused by tight supplies, before they would commit to expand. The entry of decisive competitors, however, could spoil the monopolist’s honey pot. Under threat of being pre-empted, oligopoly players would tend to invest sooner and earn less (because price thresholds are lower) rather than be left completely out of the market. Add more competitors into the market, and the threat of being pre-empted increases significantly—the competitive actions of rival firms would practically raise the risks of inaction. Thus, as markets become more competitive, firms are less likely to depend on subsidies to make their investments work.

When finance operates under an imagined world of certainty in outcomes, and markets are inherently volatile and dynamic, managers decide under erroneous bases to commit capital. Consequently, investments seldom achieve their expected outcomes. Hence, Paddy Miller, author of Innovation as Usual, questions: Why do things never turn out as they were projected? Is energy strategy always going to be a tale of unfulfilled promises?

Adaptive Portfolios as an Alternative Approach

Renewables are perceived as social goods that deliver social benefits (i.e. less pollution) while incurring private costs (i.e. higher life cycle costs). Hence, economics and policy are locked in blind alleys where subsidies become central to achieving their ends. However, the cure becomes worse than the disease when highly distorted systems emerge: expensive supplies are favored, investments are turned into rent extraction opportunities, and risks are increased when firms’ continued viability is dictated by policy actions.

In reality, renewables are among the myriad of technology choices that have economic costs and benefits. In this context, renewables are economic goods that aim to gain traction, or niches, within an evolving and transitioning energy market. This perspective leads to very different conceptions of optimality and a “common good.” In operational terms, the strategy-financeeconomics nexus, policy, and managerial roles are better apportioned. Policy sets the rules and monitors compliance, then managers make decisions and take the rewards for success or consequences of failures. This is a departure from interventionist regulatory systems: Regulators intervene and wreak havoc. Managers sift through the wreckage for “value.” Consumers ultimately pay for the misadventures with higher prices or taxes.

In this economic world, the value of renewables to a firm (or portfolio) lies in its hedge against fuel costs. Heavy front end fixed costs are incurred in order to acquire a stream of energy supplies at zero fuel costs. In contrast, ACCGT or Coal incur fixed costs, moderate operating expenses, and highly volatile fuel prices. The uncorrelated volatilities offer investors the opportunity to hedge or diversify their supplies portfolios.

More importantly, broader strategic and managerial options are made available. Under competitive conditions, with pricing and volume flexibility, renewables’ portfolio hedge value becomes apparent. To illustrate how this is achieved, let us first examine how energy prices are set.

Power (or energy) prices are set based on a recovery of fixed costs, variable operating expenses (usually proportionally small), and volatile fuel costs (such as coal or gas). When the regulator held sway in setting prices, the costs recovery is through an approved tariff set annually (or any set period). With the onset of wholesale energy markets, similar to what we see in Europe, spot prices are set by the operating and fuel costs of the marginal supply to clear demand, and a remuneration on making the supply available through a capacity fee (i.e. fixed costs).

In systems where the supply choices are coal, gas, or bunker fuels, costs “diversification” is limited. Coal, gas, or diesel prices fluctuate directly with oil prices, even if the rates vary. Renewables change the mixed supplies portfolio payoffs with their zero fuel costs. For example:

- Fuel costs are minimized when energy prices are regulated or fixed, or

- Cash margins expand when energy prices increase.

These phenomena offer a different strategic stance. In an earlier era, take-or-pay contracts were favored to secure stable cash flows to facilitate financing of investments. By fixing the volume and price commitments, one mistakenly assumes that predictable cash flows are achieved.

However, no sooner had the ink dried, market prices started to deviate from what was contracted. Take this example: To achieve stable cash flows, a buyer and seller fixed power supplies price at $0.06/kWh, with the gas supplies similarly structured, in the early days of the wholesale energy markets. When gas prices spiked, the equivalent power prices traded at $0.10/kWh. The seller foregoes $0.04/kWh while the buyer saved the equivalent amount. On a 500 MW contracted capacity, the annual volume committed is 4,380 GWh/year (500MW*24Hrs/day*365days/year*0.87). This implies a loss of $175 mln for the seller (or a gain by the buyer). When the market prices fall below the contracted price, the positive switch in favor of the seller.

In each case, foregoing the sum may be sufficient to encourage the seller (when prices are high) to renege and sell the contracted volumes to the wholesale market. This price arbitrage hardly makes the commitments stick. Hence, the repeated renegotiations that turn the contractually “secure” obligations into the very source of uncertainty.

Fiction? No, these are the common practices that consigned take-or-pay contracts to oblivion in European energy markets.

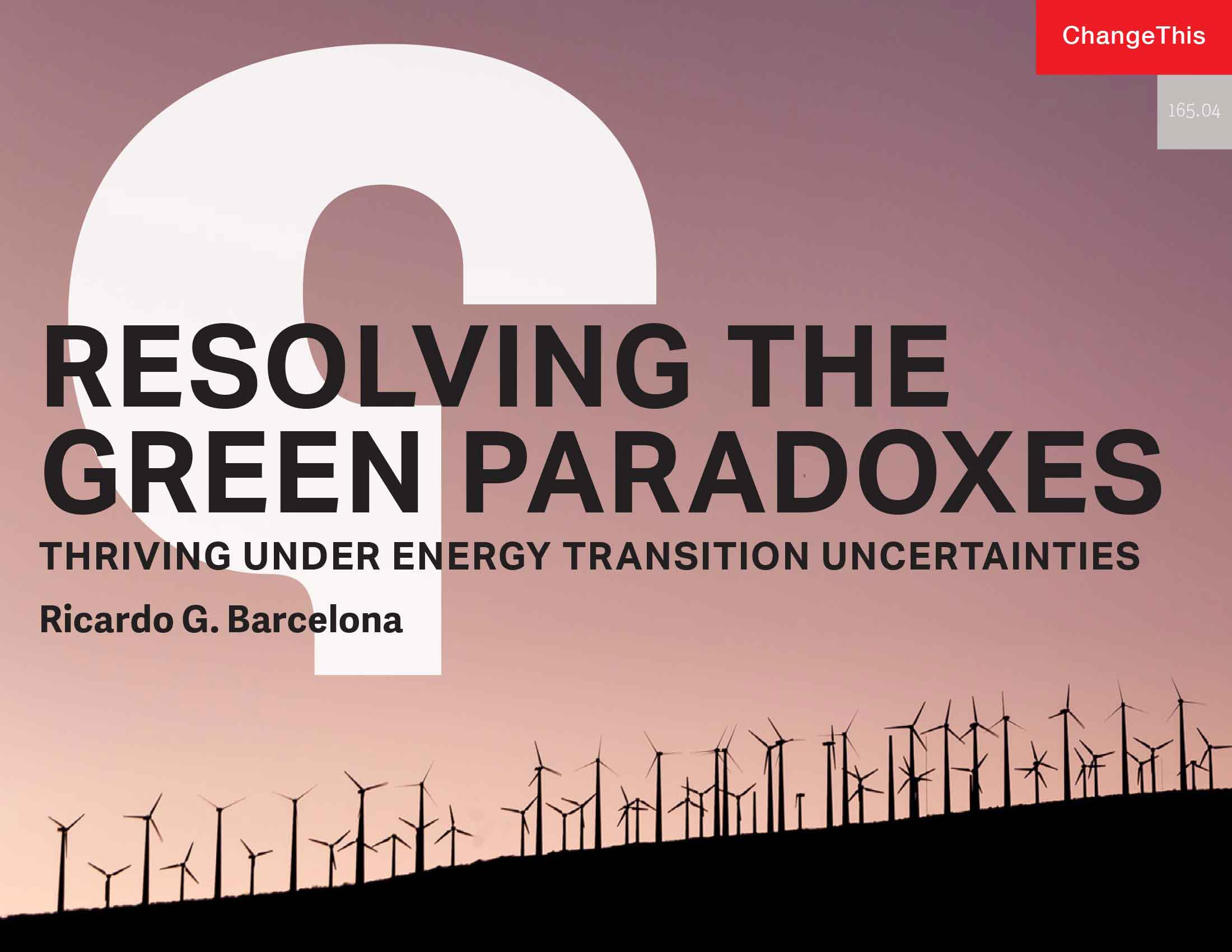

Managers could unlock renewables’ value by simulating the effects of their supply choices on payoffs and risks. Figure 1 (on the next page) presents a framework, with Chart A showing a schematic strategic tradeoff derived from simulations shown in Chart B.

Let us consider a firm that is deciding on its expansion. Managers may start with what they have—Coal (P16) or ACCGT (P15), which indexed their supplies to the market energy prices. They achieve low volatility that is rewarded with low payoffs under symmetric strategy. That is, when ACCGT (or Coal) is the price setting supply, the resulting periodic payoff is the recovery of fixed costs (1)

1. Power prices recover the fixed costs, operating expenses and fuel costs. Cash costs of supply only consider operating expenses and fuel costs. Subtracting the two, when supplies are indexed to price setting supply, cash margin equals the fixed costs recovered.

Without entering into take-or-pay contracts, stable cash flows are achieved. In reality, this was what happened in the early days of the introduction of competitive wholesale markets in Europe. With energy markets gaining adherents, and investor and financiers’ confidence grew, long term take-or-pay contracts for energy or fuels went out of fashion and ended in disuse.

With the inclusion of renewables, particular Hydro and Geo, managers are offered different alternatives to combine their Coal or ACCGTs with renewables that change the outcomes. By diversifying into renewables, cash margins expand when energy prices increase as shown by P36 in Figure 1, Chart A. Between two alternatives, P36 and P55, managers may opt for P36: It achieves substantially higher payoff at lower risks than P55. Compared to indexed strategies, P36 could compensate the increased risks with higher payoffs, following the investment logic— “higher risks, higher returns.”

Asymmetric bets take a more aggressive stance. That is, P37, P38, P41 and P56 include higher proportions of renewables to increase payoffs but talking on higher risks. This is justified when managers expect energy price trends to be upward biased (2)

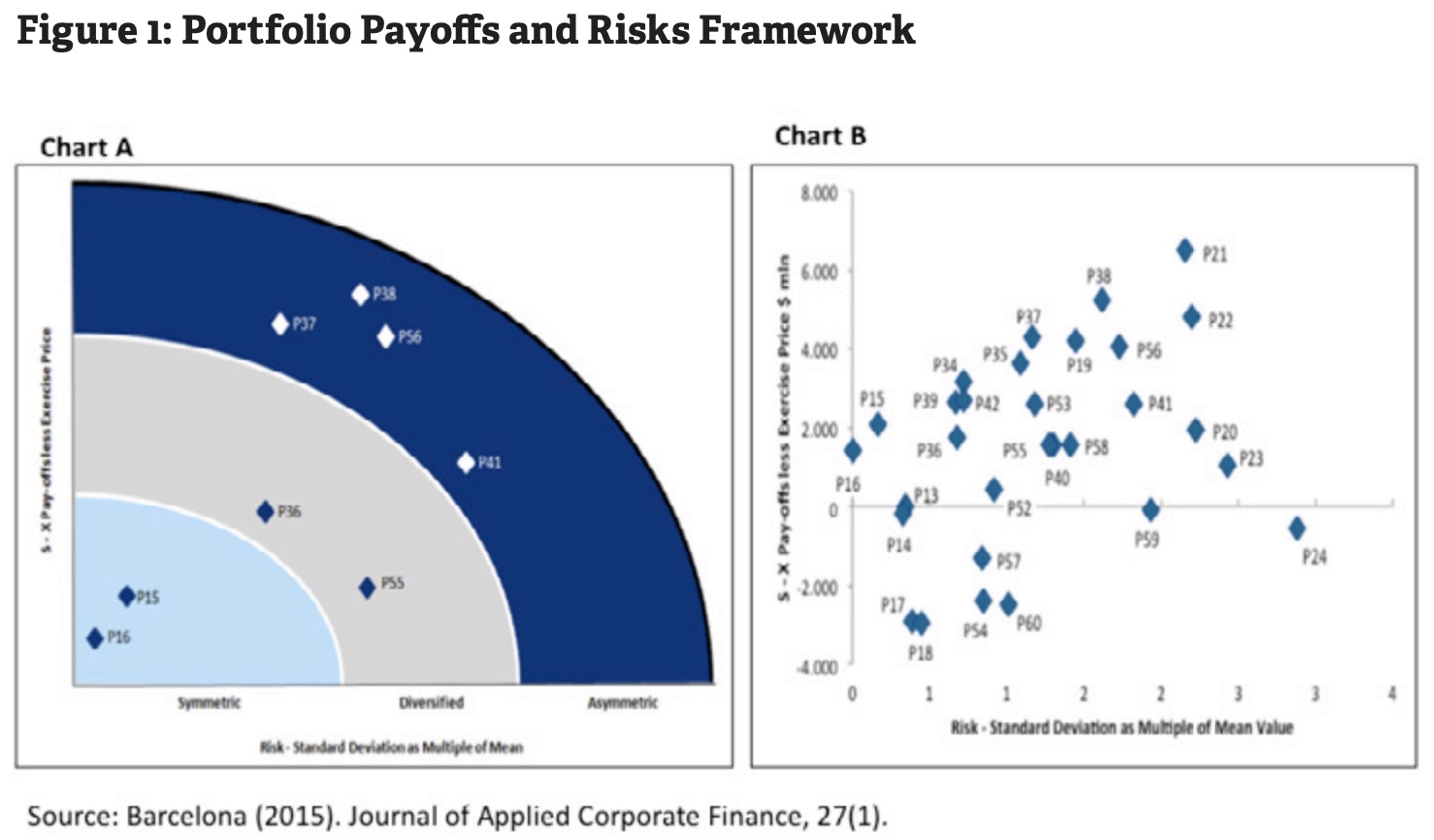

We now turn to Figure 2 to quantify the excess values delivered from diversified supplies portfolios. Under conditions of pricing and volume flexibility, the payoffs are assessed by explicitly evaluating the value impact of volatility on the portfolios considered. The excess value is simply the difference between the diversified portfolios’ value and the ACCGT-only portfolio, estimated under different energy price scenarios where ACCGTs are the clearing supplies. Three broad observations run counter to accepted energy wisdoms:

- Sequencing the coal and gas investments alter outcomes. When more cost-effective gas-only portfolio diversifies into higher costs coal, portfolio values are eroded.

- Diversifying gas-only portfolio with geothermal or hydro generally boost its value as fuel costs are partly hedged by zero fuel costs renewables.

- Onshore wind enhances gas-only portfolio values when power prices are very high, which is achieved when oil prices are above $80/bbl.

Managers often ignore the effects of sequencing of the investments on portfolio returns. One would argue, whether you invest first in Coal or ACCGT, followed by either supplies, we would end up with the same mix. However, the sequence does matter. Gas-only portfolios earn a higher return, given its lower capital expenditure compared to coal-fired generator, and lower supply costs. By adding lower return coal, the resulting portfolio may occasionally make a loss when power prices set by gas hinder coal from recovering its full costs. The result is an erosion of value.

2. The calculations behind these analyses are explained more fully in my new book: Energy Investments: An adaptive approach to profiting from uncertainties. London: Palgrave Macmillan.

How about operational flexibility, and the risk of non-dispatch of expensive supplies?

Let us recall how the wholesale energy market works. To determine which supplies are periodically dispatched, the available supplies are stacked from lowest to highest marginal cash costs (i.e. operating expenses plus fuel costs). The supply that clears the demand sets the price, while any supplies with costs above this price are not dispatched. Financiers look at this as a risk because volumes not sold do not generate revenues or recover their costs (i.e. fixed costs).

This perspective fails to appreciate how the competitive energy market has reframed the riskspayoffs from the days of highly regulated regimes. Here is the market reality:

When a firm offers to supply, they premise their actions on earning a cash margin. Without the obligation to supply, even at a loss, competitive markets attract the right volumes to be supplied vary prices according to the supply—demand available at the time. This market system offers the supplying firms sufficient scope to decide when to supply, and on a strategic level, what mix of supplies to choose to meet what they expect the future market would need.

Managers of course could misjudge the future. For this reason, they may hedge their bets by opting for a diversified supply portfolio. They could retain operating flexibility, by opting for flexible prices and volumes, to adapt their supplies decisions according to how the energy market would evolve.

Consider a supplying firm that operates under the following strategy:

When cash costs of supply exceed the power prices, the firm opts to interrupt supplies to avoid making a loss. In effect, this is what happens when supplies are not dispatched because firms offered prices that are above the marginal costs of the price-setting supply. Renewables’ zero fuel costs would secure its place given its lower cash costs of supply, hence securing its supply whenever it is available to supply the energy markets.

By implication, expensive supplies become stranded when they are consistently left out of the energy market. More subtly, as cheaper sources substitute expensive supplies, as in the case of ACCGT replacing Coal, energy prices would tend to decline (as they did) when competition was introduced in Europe. In turn, the inclusion of renewables, particularly hydro and geothermal, when prices are not distorted by subsidies, energy prices would vary more according to the variations in renewables’ supplies.

For renewables, the problem is not one of dispatch. It is earning enough payoffs to justify the higher capital expenditure needed to make the supply available. By keeping prices flexible, they earn higher payoffs when energy prices are higher. In the absence of fuel costs, any increment in energy price is accretive to cash earnings (or vice versa). In effect, renewables’ advantage of low cash costs of supply is offset by generally higher asset costs that need to be fully recovered to make the investments worthwhile.

These observations contradict the belief that non-dispatch represents a risk by foregoing revenues from volumes that are available. This is worth a reminder: Value is created by cash margins, not by revenues. Earning revenues while making losses erode portfolio value, as coal experienced in several competitive energy markets that gas came to dominate.

Correctly valued, renewables’ contribution to portfolio values question the need for subsidies to propel their wider deployment. Under transitioning energy systems, inclusion of renewables form part of a calculated move by firms to thrive under greater price and volume volatilities, and uncertainties of outcomes. Without the distortions from subsidies, managerial decisions could be made under economic rationale where profits and societal benefits coalesce to form sustained transitions to lower carbon economies.

The Sun Can Wait: Late-Movers’ Advantage

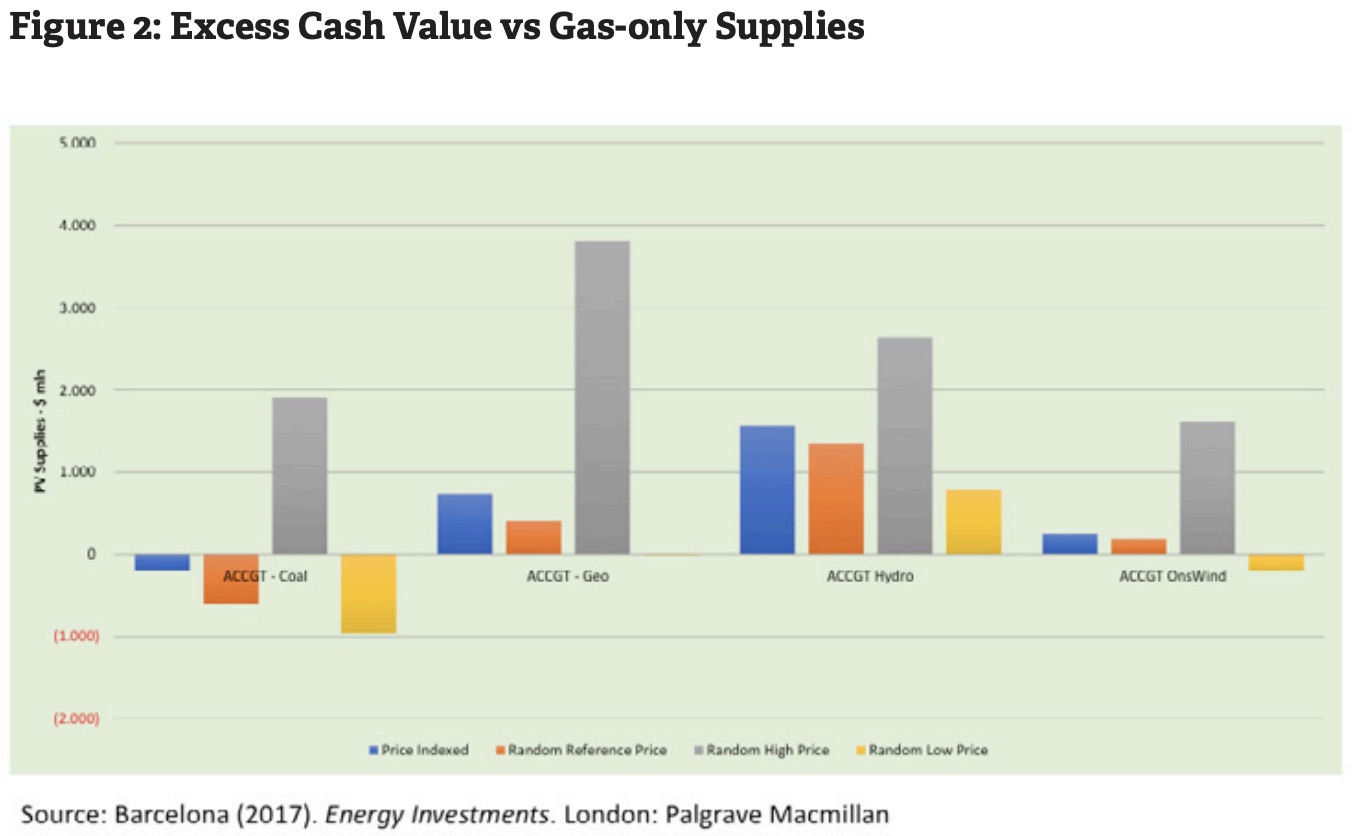

Solar power attracted media attention, partly inspired by its rapid capacity expansion in China and the United States. The argument follows this logic: Learning curves suggest that with each doubling of installed capacity, costs of solar would fall by 20%, as shown in Figure 3 (Learning Curve—PV). This premise influenced policy to focus on volume growth by sweetening the deal with generous subsidies. However, this is the seed of the policy’s failure. Once subsidies were cut, as Spain, Germany, as well as other Europeans did, deployment stood still leaving in its trail bankrupt developers. How did such benevolent policies fail to deliver?

This brings us to the latecomers’ paradox, a reversal of strategy’s mantra of a first-movers’ win by the bold and the brave.

The first mover (Figure 3—First Mover—PV) is locked in with “expensive” assets. As costs fall, the early movers’ assets are rendered obsolete by technological advances. This could result in one of two scenarios: a) Subsidies increase over time to close the gap; or in its absence, b) losses spike because of under-recovery when payoffs prove insufficient to recover capital expenditures. Under these conditions, managers may decide to invest now or wait until equipment costs have fallen farther.

By waiting, investors forego say two or three years of revenues. In a year, there are 8,760 hours (24 h/day x 365 days/year) available to any power generators. Optimistically, at 22% conversion rate, a kW of solar capacity produces 1,927 kWh a year. For every kW of capacity, the revenue loss is about $134 (or $269 for two years, $402 for three years). Deduct the high—low ranges of operating costs from $95 ($0.0495/kWh * 1,927h) to $28 ($0.0146/kWh*1,927h), the annual cash margins are between $39 and $106 (or $78 to $212 for two years, $117 to $318 for three years).

Solar’s installed costs range from $1,500/kW to $1,000/kW, with some suggesting below $1,000/ kW. This is a far cry from $4,000/kW to $5,000 kW as recent as 2010. Managers looking at this data would do this quick math: solar costs should fall less than 5.2% to 21.2% in two years, or from 7.8% to 31.8% over three years. With advocates suggesting a more drastic fall, waiting two or three years could prove more lucrative. On a more realistic note, power prices fell from its peak in 2008 to settle at lower levels when oil prices fell from $140/bbl to less than $40/bbl before rebounding to $70/bbl. To make solar financially viable, it is racing against the pace it succeeds in reducing costs, and the rate oil prices erode its benefits.

While coal is presented as the epitome of what is wrong with today’s energy, energy prices under coal-dominated systems tend to be higher, hence friendlier to solar power’s economics (Figure 2: Deferral Value—Coal Static Volume). Under very high (++), high (+) or low (-) power price scenarios, the late-movers could achieve positive portfolio values by virtue of the higher energy prices. The early mover, in contrast, could only contribute positively when energy prices are very high (++). Consequently, deferring actions could offer the prospect of lower capital outlay and higher positive payoffs.

Gas’s dominance shifts the energy prices lower, given ACCGT’s lower supply costs. This implies a squeeze on Coal and Solar power’s revenues (Figure 2: Deferral Value—Gas Dynamic Volume). Solar’s financial prospects drastically deteriorates under all price scenarios considered. Solar could only survive financially with large injections of subsidies or the willingness of altruistic consumers to pay above market prices to sustain their viability. In this case, managers would rather wait. Under highly subsidized regimes, its longevity would depend on how long payments are sustained under increasingly hostile political contexts. As consumers realize that Solar investors take little financial risk, while kept afloat at their expense, consumers would coax regulators to cut subsidies.

The narrative for Solar changes for isolated energy markets. Without interconnections of infrastructures to accept fuel deliveries, communities may have to rely on small hydro, geothermal, or solar power. Perhaps, this is where the niches for Solar could be established more securely. Economics become a conversation around the costs of not having access to energy, rather than the costs to deliver. With this reframing, the economic and social costs of gaining access to energy appear to converge more closely. Thus, the situation of pushing “expensive” Solar supplies to well-connected markets, reverses itself into a pull for bridging energy supplies that Solar could well satisfy.

These are possible areas where micro-grids, battery storage, and similar emergent technologies could be tested and deployed. Where they are deployed is a question of matching what else is available, and what the communities could affordably absorb.

Making Economic Choices Work

Strategy is formulated from hypotheses of what the firm is, what it can be, and how best its resources could be augmented or deployed to gain their niche in an ever-evolving market. This is what Richard Rumelt, described as the strategists’ strategist, prescribes in his book Good Strategy, Bad Strategy. In effect, decisions and energy choices are contextual. The context being how malleable the markets are to allow managerial actions, policy, and consumers interests to coincide, to interact to shape how energy transitions may progress (or retrogress). In effect, markets and their structures, created by human interactions, are prone to influence by managerial actions that seek to uniquely appropriate the fruits of their labor and risk-taking.

Following this logic, to achieve or even accelerate the energy transitions—and profit from it—policy’s interests and roles are specific: they ensure the continued viability of the energy markets as arbiter of value in allocating resources. This requires a move away from nurturing the addiction to subsidies by letting managers navigate the uncertainty of markets, take risks, and reap its rewards or incur its penalties.

Emergent technologies are supported through access to research and development infrastructures, where talent and ideas are incubated. Access to funding is made possible by creating a “market” for ideas where financiers could interact with start-ups. This recognizes that policy and managers share a common limitation: neither is endowed with omniscience to know where the experiments would lead. Where policy often lacks flexibility, managers tend to have greater scope to reverse or accelerate the pace of their actions. This is what makes firms more agile where the ability to create and play in profitable market niches spell the difference between financial viability or failures.