The Stories We Tell About Money

After a career in nonprofit youth work, I became a financial planner.

I went from thinking money strategy was for “not for me” to guiding thousands of 1-on-1, confidential conversations with all sorts of people. After just a year, I realized I wasn’t creating the change I sought. I was swimming against the current of misinformation, distracting consumerism, and institutional bias.

Most people are engaging with financial planning on a silo, transaction-level basis because most financial professionals come from a business, accounting, or sales background. That may or may not make sense in the context of their lived experience; individual results may vary.

Most financial content is of the “I made millions and you can too” influencer variety or technical articles interesting only to the author. And most people I spoke to didn’t connect with them either. Mindset books completely ignore our history, as if all of us are starting the race from the same line, without headwinds or tailwinds.

Finance is focused almost entirely on the financial outcomes; however, those outcomes are built on the foundation of relationships. Information is only as valuable as our relationship to the source. Sometimes we get problematic advice from someone we trust while disregarding excellent advice from someone we don’t. And many of us just “don’t like” numbers.

But a personal story, when I could speak from the heart and allow them to compare my experience with money to theirs, was well received.

We are all influenced by our own stories and the collective stories that we tell, which is why for finance to be relevant, it must first be cultural.

In my book Change From Your Dollars, I offer stories about money, not statistics.

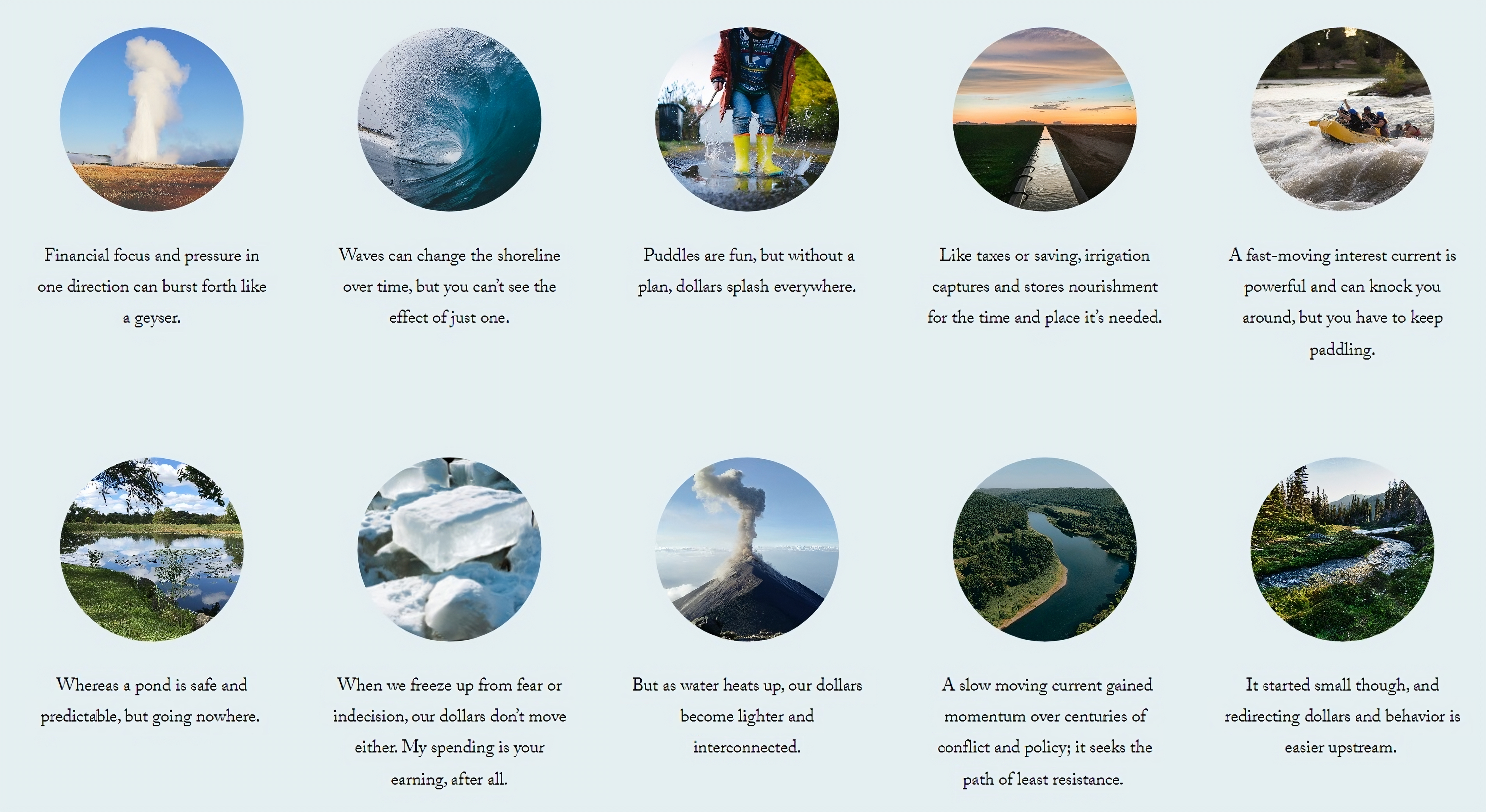

Many people turn to numerical articles or anything relentlessly logical when we are all affected by money as much as we are all affected by water. The principles of math were derived from observation of our natural world.

Throughout the book, I compare money to water, as they behave in similar ways:

Change from your dollars is created through informed action and decision. You don’t need to be an expert to be informed, but you do need to acknowledge reality: the good, the bad, and the ugly. We can only heal when we acknowledge what is.

Money doesn’t exist “apart” from our lived experience, “over there.” It is a proxy for our energy, good or bad. The financial rulebook isn’t taught well (or at all) because it’s a game: opting out has consequences. Reform is absolutely possible. After all, reality is shaped by money, and money is shaped by perception, so … let’s change our perception.

As I talk to business owners and nonprofit executives around Milwaukee, we note how the spaces we occupy are labeled against our will. We as people, as organizations, don’t feel “for profit” or “not for profit”. Each hour of each day, I am given choices. Some are profitable and others are not. Some might be profitable 20 years from now. Others are goodwill mental health profit. It’s too multifaceted to measure in a day.

But no dollar is neutral. Every dollar has a social impact.

We can create change from our dollars, improving connection and access for all. Money is a construct, and it’s used by Oprah and Putin and you and me. The difference is that if you start with a scarcity mindset, you create a win-lose view of life, but if you think abundantly, we can care for everyone. After all, socialism is about sharing, capitalism is about creating, and we all want some of both.

Imagine a river, its current reflecting our collective energy and intention in all things. Democracy is messy, but a healthy democracy is always adapting, just as a river current will become fast or slow, deep or shallow, depending on the environment.

A river begins as a small, trickling, stream. It just needs time to get going. Upstream investments, like snowmelt in the mountains, almost always yield results if we have the patience to wait.

Examples I outline in the book include, decoupling property taxes and public school funding, funding preventative healthcare, public transportation for all, and limiting fundraising in politics.

Easy? Of course not. But the financial winners of today tend to maintain the status quo, because adapting to change is a hassle. They can afford to privately pay everything when public services fall short. But don’t we believe all children in America deserve the chance to thrive? We all can do our best work when our basic needs are met.

Streams converge into rivers and form deep channels and roaring rapids, representing the momentum begun earlier in the mountains. It’s harder to go against the current downstream… Resistance is more likely, total reversal nearly impossible.

Downstream incentives steer our direction after the current has picked up speed. Not so long ago, for example, many people had never heard of organic food, which is now mainstream. Now consider all the tax credits and deductions, carried interest taxation, subsidized loans, grants for energy efficiency/historical preservation/electric vehicles/hiring practices, and a whole bunch of things many of us never think about that nonetheless shape our behavior. These are affected by voting and consumer behavior.

Downstream incentives call out our role as referees in the game of money: the public and the private sector need our dollars to exist. They work for us, not the other way around. The rulebook can change.

So stop doom scrolling and take small, consistent, incremental action. When we focus on the social impact of our dollars, we are more intentional consumers and voters. Capitalists brought the personal computer and socialists fought for the weekend. It’s always both.

That’s how change from your dollars happens in your neighborhood, city, world. How about the work within, in our psyche? We must change our perception to change our reality.

People with very different stories and very different personalities are able to achieve positive financial security. When someone tries to chase other people’s examples and anecdotes, they get tired trying to be something they’re not. They might be putting in the effort, but if the effort isn’t aligned with a pathway that they can deliver on, there will be a tension and fatigue that makes chasing money not worth it.

Drawing from thousands of confidential conversations and in sharing my own stories in the book, I describe four behavioral pathways to getting good financial outcomes.

Clients don’t share one story or one pathway. As a group, they share patterns and overlap. It’s easier to build on an existing strength than try to reinvent yourself to cover a weakness.

Rate of Rejection

ROR also stands for rate of return, and there’s a very strong correlation between that and rate of rejection. In order to win you must risk a loss. If you’re in the arena, playing the game, your skills will improve over time.

Risk of rejection is the most external pathway, because absorbing rejection isn’t easy. The community organizer and sales rep alike get brushed off. The actor might bomb the audition. The attorney might lose a case in court. The political candidate might become a punchline for millions.

So much of mindset coaching is focused on accepting and learning from failure. Hard to do, since we all want to be accepted. Compensation tends to reward people that do what others don’t want to do: be rejected and perform under pressure.

This is the immigrant story: leave everything you know and start over at the bottom. It’s the critical point of almost every Disney movie: it tests what we’re made of, and how important the goal really is.

This pathway doesn’t require imagination, but it does require persistent visualization of success. And thick skin is a must.

Grow Your Gift

Think big, but start small. Growing your gift means putting in the practice long before any performance, opening, or sale. We all have gifts, but gifts need to be nurtured, not neglected.

A person sharing their gift is likely to find financial abundance once it is magnetic enough. A performance or a business can scale, that is: a gift has been developed enough to create a multiple of demand. The open mic night becomes a theater, the high school gym becomes a sold out arena. But often growing your gift is more subtle. Not everyone is a performer or inventor.

Your gift is a unique ability or insight and it may be hiding inside your job description. What part of your job do you love and excel at, and how can you spend more of your time doing that? Gifts are grounded in abundant thinking. Grow them with vision, focus, and faith. (That said, gifts can be destructive when grounded in scarcity thinking, like fear-based messages.) A unique gift offers more to the receiver than they pay in return.

This pathway doesn’t require balance or harmony. It’s often the opposite, a meteoric obsession that leaves collateral damage. That’s why rock stars need managers and dictators need a military.

Buy What You Use, Use What You Buy

Be intentional. A good result of capitalism is a well made product that fits your needs perfectly. A bad result of capitalism is buying something you won’t use because of manufactured feelings of inadequacy. This pathway is all about knowing yourself, detaching from social comparison, and recognizing the difference above.

Some products are made cheaply and break easily, but many like furniture, cars, bikes, and even clothes, are made to last a long time. The longer you keep cars, furniture, clothes and the more you use them, the more dollar value extracted. It’s a strong case for minimalism. The empty guest room was bought but isn’t used. The home gym is collecting dust. Oh, and interest charged on financing is always frontloaded. The seller of a product or provider of a service has to be ready to deliver when you want it. The seller has already committed, you the buyer must also commit to get full value.

So, changing your mind always has a cost. FOMO will undercut this pathway, always chasing a shinier, newer thing. Ownership is for unlimited use. We pay for quality, so make sure you love it or need it. Or love it so much you need it.

This pathway doesn’t require much rejection, just remember you can’t keep up with the Jones’s on everything. But it does ask for a lot of reflection: What do I really like and why?

Compounding Actions

A lot has been written about habits. Starting a new one is nearly impossible, and so is breaking an old one. Simple things like saving, situps, and salads have a powerful effect on our lives when compounded day after day, month after month, year after year. Simple, but hard, especially at the beginning! As Les Brown said, “do what is easy and your life will be hard.”

Compounding builds over time, accumulating power like a river current or an avalanche. Thirty-minute workout 5x per week or one two-hour Saturday? $50 per month for five years or $2,500? Small actions done well consistently add up. This pathway is the most internal: habits are all about discipline in action when no one is looking.

But complex forces compound over time as well: wealth and trauma alike are usually passed generationally. Systems influence compounding for better or worse, because systems steer us to the path of least resistance, like a river current. It could be tax laws, auto-transfers, or a meal planning service; all build habits. Changing course is hard, maintaining momentum is easier. Getting started is the hardest.

This pathway doesn’t require much unique insight, in fact it’s grounded in conventional wisdom millennia old.

The first two pathways above all acknowledge the math of compensation in our economy: people are rewarded when they have a unique insight, ability, or gift they can share, or, when they are willing to do something most people just won’t voluntarily do. The former includes athletes, artists, and entrepreneurs. The latter includes executives, doctors, and financial planners. The former involves a lot of frontloaded cultivation, thinking, and sweat. The latter involves a lot of discipline, stress, and performance under pressure. At the highest performance levels, all the above is required.

The second two pathways explain how financial abundance can find those who don’t earn as much or take big risks. After all, things tend to work out when you earn more than you spend.

What can you do?

Reflect on which pathway(s) to financial wellness suit you and seek to align your actions. Let go of being someone you’re not. There’s easy money to be made by convincing a mass audience that this is “the one thing” that’s between you and money windfall. The closer to our heart, or our deepest desires and fears, the more likely we are to make a change. Everybody worries and wants, but fear and desire are the catalysts for change.

Register to vote and engage in local politics. Think globally, act locally. It’s overwhelming to change in the big wide world. Being informed isn’t much use if you aren’t acting on it. Contact your local representative and ask how to get involved or what they’re working on. Volunteer with a nonprofit and get their policy positions. Great things are happening, and there’s always more hands needed.

Find a handful of friends you trust and form your own “board” in order to have a confidential, personal source of financial perspective and feedback. A board leverages multiple lived experiences, skills sets, and perspectives. Even if you don’t get answers, you’ll feel better sharing out loud. The primary barrier to financial wellness is often a barrier to connection. A finance professional might be dismissive of the role of trauma in your life and in our nation. A lack of acknowledgement makes it harder to heal. You might find it hard to communicate with an advisor because we increasingly socialize with people in similar situations, so building rapport across socioeconomic strata becomes harder. And this being America, we subconsciously correlate a person’s dollar value with their human value, which is an insidious lie. Speaking openly with friends is a good first step.

Get in touch with me to explore how we can collaborate here in Milwaukee and beyond. Cognitive biases, the compounding effects of wealth and poverty, and the effect of a safety net on risk tolerance all affect how we make financial decisions in our lives, at home and at work. I provide consulting and speaking services to assist you in making sound financial decisions.

Finally, read and share the book! You’ll get accessible insight from a practitioner into how actual people, and more on how public policies and private perceptions shift the current of money. You’ll read stories of personal cause and financial effect, all without judgment.